Disintermediation

Diagnosing disintermediation in insurance comparison platforms and reframing the product around trust and user autonomy.

OVERVIEW

Diagnosing disintermediation in insurance comparison platforms and reframing the product around trust and user autonomy.

Thesis

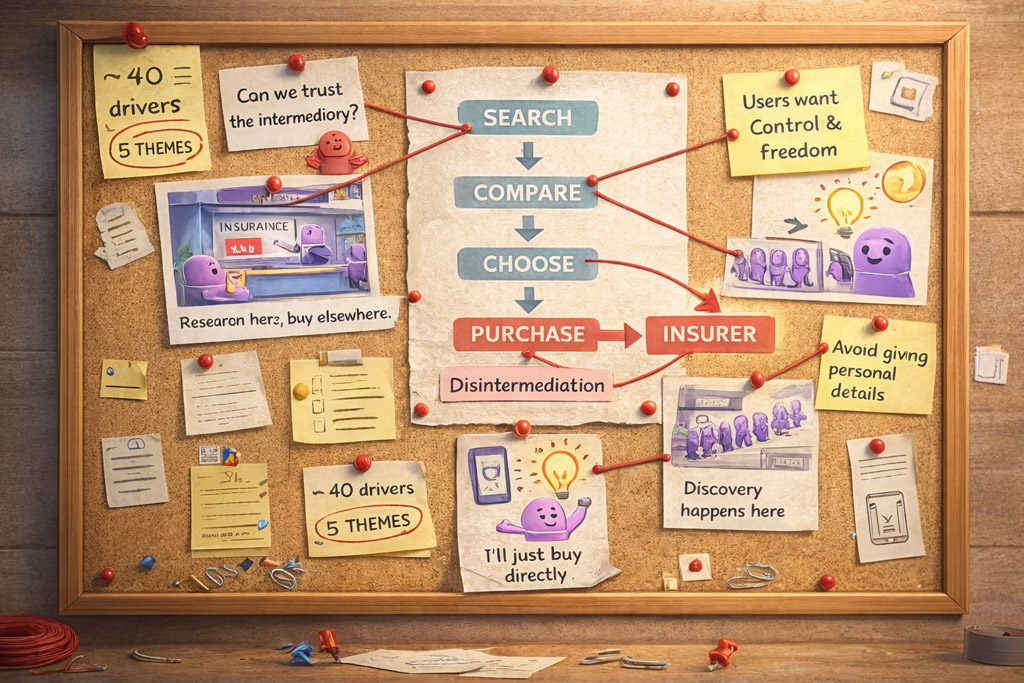

Insurance comparison platforms often win the moment of search but lose the moment of purchase.

Many users use these platforms to explore the market, then purchase directly from insurers. This behaviour, known as disintermediation, points to a deeper issue than funnel friction alone.

At Compare Club, I investigated this pattern and reframed the problem from conversion optimisation to one of trust, transparency, and user autonomy.

This work laid the foundation for repositioning Compare Club from a sales intermediary into a trusted financial advisor.

The Problem

Internally, the low conversion rate was largely framed as a funnel optimisation problem. The assumption was that users were abandoning the journey due to friction in the comparison flow, such as complex forms, unclear options, or insufficient guidance during the purchasing process.

As a result, most discussions focused on improving the mechanics of the funnel: simplifying inputs, refining the sequence of steps, and encouraging users to submit their contact information so sales people could assist them.

However, early signals suggested that the issue might not be purely operational. Many users appeared to be using comparison websites primarily as research tools, gathering information before completing their purchase directly with insurers.

If this was the case, the challenge was not simply about improving conversion inside the platform; it was about understanding why users chose to leave the intermediary entirely at the moment of purchase.

This raised a deeper question:

Why do users begin their journey on comparison platforms but ultimately choose to buy directly from insurers?

Answering this question became the focus of the research that followed.

Context

Compare Club operates as a digital comparison platform that helps Australians evaluate and purchase insurance products from multiple providers.

The platform is highly effective at attracting users at the beginning of their insurance journey, but many customers use comparison websites primarily as research tools before completing their purchase directly with insurers.

Internally, this behaviour was visible through a relatively low conversion rate from research to completed purchases, estimated at approximately . This created a significant gap between the platform’s ability to attract potential customers and its ability to convert them into policyholders.

At the same time, the company had begun exploring initiatives intended to strengthen its relationship with customers beyond the initial purchase, including a product concept called Club+. However, the role and value of this product within the overall customer journey remained unclear.

My role was to investigate why users were leaving the platform before purchasing and identify opportunities to strengthen the platform’s position in the insurance decision process.

Research Objective

To understand the drivers behind disintermediation, I initiated a research study focused on users who began their insurance journey on comparison websites but ultimately completed their purchase directly with insurers.

Rather than focusing on improving funnel mechanics, the goal of the research was to investigate the behavioural and perceptual factors that led users to abandon the intermediary at the moment of purchase.

The study aimed to answer two core questions:

Why do users research insurance on comparison platforms but purchase directly from providers?

What would make them comfortable completing that purchase on the platform?

Understanding these drivers would help determine whether the solution lay in improving the purchasing flow or in redefining the role the platform plays in the insurance decision process.

Research Design

The study was designed as a series of qualitative interviews with insurance buyers who had recently researched policies on comparison websites but ultimately purchased directly from insurers.

Participants were recruited shortly after completing their purchase to ensure that their reasoning and decision-making process was still fresh.

To better understand behavioural differences, participants were grouped into two broad profiles.

Users who conduct extensive research before making a purchase decision. They often use comparison websites to narrow down options, but prefer verifying details and completing the purchase directly with insurers.

Users who tend to remain loyal to existing providers and rely on comparison platforms primarily to validate their current policy rather than actively switch insurers.

Interviews focused on reconstructing the decision journey step by step, identifying the moment when users chose to leave the comparison platform and purchase directly with the provider.

Participants were asked to describe:

how they began their insurance search

how they evaluated options on comparison platforms

when and why they decided to leave the platform

what would have made them comfortable completing the purchase there

This approach allowed us to capture both the behavioural triggers and the perceptions of trust, transparency, and control that influenced disintermediation.

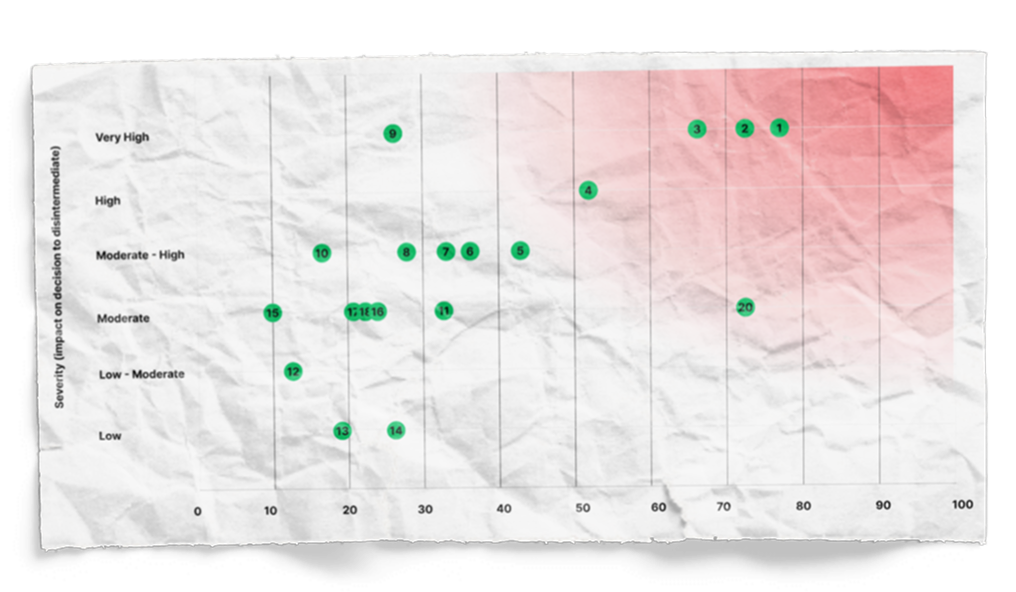

Synthesis: Drivers of Disintermediation

The interviews surfaced reasons why users chose to leave comparison platforms before completing their purchase.

Across the study, these signals were synthesised into themes that explained the broader causes of disintermediation.

Rather than treating these as isolated usability issues, I used them to identify the deeper tensions between how comparison platforms operate and how users prefer to make financial decisions.

Of the themes that emerged, two proved especially important in shaping the product direction.

Trust and transparency

Many users wanted greater confidence that the platform was acting in their best interest and presenting information in a way that felt clear, unbiased, and reliable.

User autonomy and control

Users wanted to explore options on their own terms, verify information independently, and avoid feeling pushed into a sales process before they were ready.

Key Insight

Across the interviews, one pattern became clear: users were not leaving comparison platforms because they struggled to use them.

They were leaving because they did not fully trust the intermediary at the moment the decision became consequential.

What they wanted was not just a simpler funnel, but a clearer sense of control, transparency, and confidence in the decision they were making.

This shifted the challenge from optimising a sales journey to designing a trusted decision environment.

Two principles followed from this:

User autonomy and control

Users want to research, compare, and verify insurance decisions on their own terms, without feeling pressured or constrained by the platform.

Decision support

Rather than acting primarily as a sales intermediary, the platform needed to help users make better financial decisions by offering guidance, clarity, and transparency.

Together, these principles reframed the product from a transaction tool into the foundation of an ongoing advisory relationship.

Strategic Reframe

The research suggested that improving conversion would require more than refining the comparison experience.

If users fundamentally questioned the neutrality, transparency, and incentives of comparison platforms, then optimising the purchasing funnel alone would not solve the problem. The platform needed to build a stronger foundation of trust and demonstrate that its role extended beyond facilitating a transaction.

This insight reframed the strategic role of the product.

Rather than acting primarily as a sales intermediary, the platform needed to evolve toward becoming a trusted financial advisor — helping users understand their insurance decisions, evaluate options more confidently, and manage those decisions over time.

Within this reframing, Club+ began to take on a clearer strategic role.

Originally positioned as an additional product experience, its purpose had remained ambiguous. The research revealed an opportunity to reposition Club+ as the place where the ongoing relationship with users could live — supporting them beyond the moment of purchase.

Instead of focusing solely on helping users choose a policy, the platform could begin helping them navigate insurance decisions throughout their financial life.

This reframing opened the door to exploring how the product could support users not only at the moment of comparison, but also in the months and years that followed.

Design Direction

If the platform was to act as a trusted financial advisor, it needed to support users beyond the initial purchase.

Insurance decisions do not happen once. They evolve as people’s financial situations, health needs, and life circumstances change. Yet most comparison platforms are designed around a single moment: helping users choose a policy and complete a transaction.

The research pointed toward a different model.

Rather than treating insurance as a one-time purchase event, the platform could begin supporting ongoing financial decision-making through lighter, more continuous interactions over time.

This line of thinking started to reshape how I viewed Club+. Instead of existing as a static dashboard or document repository, it began to suggest a broader role: a place where the relationship with users could continue after the moment of purchase.

That future direction became important enough to evolve into a separate body of work.

I explore that idea more fully in the next case study, where Club+ becomes the foundation for a more proactive and lightweight model of financial guidance.

Organisational Change

Implementing this shift required more than product design. It required gradually changing how the organisation thought about its relationship with customers.

Historically, the platform had been optimised around lead capture and sales conversion. Many of the interaction patterns in the funnel were designed primarily to collect user contact details and connect them with sales agents.

The research highlighted how these patterns conflicted with what users actually wanted: control over their research process, transparency in pricing and options, and freedom from unwanted sales pressure.

Changing this model could not happen overnight. It required sustained internal work to shift the conversation from short-term sales optimisation toward building a more trusted relationship with users.

Over time, several incremental changes began to move the platform in that direction.

Within the comparison experience, the team started exploring ways to simplify the funnel and reduce friction in the early stages of research. One of the more significant discussions involved reconsidering the lead gate, allowing users to explore and interact with results without immediately providing personal details.

At the same time, Club+ began evolving away from a static repository of policy documents toward a more action-oriented experience that helps users understand what they should do next.

While these changes were gradual, they represented an important shift: moving from a system designed primarily to capture leads toward one designed to support better financial decisions.

Reflection

This work revealed that disintermediation was not simply a usability problem. It was fundamentally a trust problem embedded in the intermediary model.

Users were willing to use comparison platforms to explore the market, but many still preferred to verify information and complete their purchase directly with insurers when the decision became consequential.

Addressing this behaviour required more than improving the mechanics of the purchasing funnel. It required rethinking the role the platform plays in the insurance decision process.

The research reframed the opportunity from optimising a sales interaction to designing a system that helps people understand, evaluate, and manage their insurance decisions over time.

This shift laid the groundwork for exploring how Compare Club could evolve from a comparison tool into a trusted financial advisor for its users.

Edgar held the role of Head of Customer Experience at Compare Club between 2024 in Sydney, NSW.